Table of Contents

Introduction

I’ve been working my way through Fraud and Fraud Detection (Gee, 2014), a 2014 book by Sunder Gee intended for accountants and auditors (but valuable to the rest of us!) The book goes through statistical tests that can be used on sales, purchases, expense reports, payroll, and other data sources in order to detect fraud.

Most of the examples depicted use IDEA Audit software by CaseWare since this software is used by actual forensic accountants, but you don’t need this software to apply the techniques depicted.

One of the most interesting techniques is Benford’s Law. This concept is defined as:

A law discovered by Dr Benford in 1938, which shows that in sets of random numbers, it is more likely that the set will begin with the number 1 than with any other number

(A&C Black, 2007)

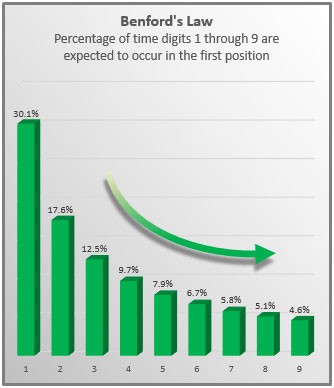

Benford’s Law

Essentially this law states that certain numbers (especially 0 and 1) are more common in numerous “normally distributed” datasets. You can see the chart to the right (Collins, 2017) indicating the general proportion of these digits.

You can use Benford’s law – where it applies – to identify fraud by exploiting our natural tendency to invent the same numbers that do not follow this distribution.

We know that humans are not good at selecting random numbers (Towse, Loetscher, & Brugger, 2014) and this results in the eventual violation of the law over the course of a dataset.

Examples of Applying Benford’s Law

Benford’s Law has been used to detect fraud in sales data – for example if you are inventing fictitious sales to launder money you are unlikely to conform to Benford’s law and this can be detected across a large enough data set.

It can also be used to detect fabricated data in scientific studies (Hüllemann, Schüpfer & Mauch, 2017) In that study, it successfully identified 100% of the known fraudulent articles.

{kind=link}

Criteria to use Benford’s Law

There are some criteria that must be met in other to use Benford’s law. These criteria are (Gee, p. 69):

- The numbers should all describe the same object (e.g. sales, invoices or income) – not mixed

- There should be no minimum or maximum inherent in the data

- The numbers should not be assigned, like telephone numbers

- The numbers should not be uniform distributions like lottery balls where the balls themselves are selected and not the numbers

Additionally, you should have an understanding of the data. For example, the book gives the example of car dealership sales where they have a spike of sales in the $20,000-30,000 range, except that this is the general sales price of the car. For this reason, a violation of Benford’s law is to be expected.

Pitfalls to Benford’s Law

Benford’s law is merely a first step in your data analysis. It cannot alone indicate fraud. As we saw with our auto dealer example, if you don’t understand your data you can make incorrect predictions.

In particular, Benford’s law cannot be used to determine election fraud. (Brown, 2012; Dckert, Myagkov & Ordeshook, 2011). Votes do not follow the expected pattern required for Benford’s law to be effective – and this has been confirmed by looking at both elections where elections have been found to be conducted fairly and known fraudulent elections.

Conclusion

Benford’s law is a useful tool for accountants, auditors, data analysts, data scientists and others who may need to identify unusual patterns in their data that may indicate the potential of some kind of fraud or misappropriation.

References

Benford’s law. (2007). In S. M. H. Collin, Dictionary of accounting (4th ed.). A&C Black. Credo Reference: http://ezproxy.eastern.edu/login?url=https://search.credoreference.com/content/entry/acbaccount/benford_s_law/0?institutionId=2600

Brown, M.S. (2012) Does the application of Benford’s Law reliably identify fraud on election day? Master’s Thesis, Georgetown University. Retrieved on May 2, 2021 from https://repository.library.georgetown.edu/bitstream/handle/10822/557850/Brown_georgetown_0076M_11716.pdf

Collins, J.C. (2017) Using Excel and Benford’s Law to detect fraud. Journal of Accountancy. Retrieved on May 2, 2021 from https://www.journalofaccountancy.com/issues/2017/apr/excel-and-benfords-law-to-detect-fraud.html

Deckert, J., Myagkov, M. & Ordeshook, P.C. (2011) Benford’s Law and the Detection of Election Fraud. Political Analysis. 19:245–268. doi:10.1093/pan/mpr014. Retrieved on May 2, 2021 from https://courses.math.tufts.edu/math19/duchin/dmo.pdf

Gee, S. (2014) Fraud and Fraud Detection. Hoboken, NJ: Wiley.

Hüllemann, S., Schüpfer, G. & Mauch, J. (2017) Application of Benford’s law: a valuable tool for detecting scientific papers with fabricated data? : A case study using proven falsified articles against a comparison group. Anaesthesist. 66(10):795-802. English. doi: 10.1007/s00101-017-0333-1. PMID: 28653153.

Towse, J. N., Loetscher, T., & Brugger, P. (2014). Not all numbers are equal: preferences and biases among children and adults when generating random sequences. Frontiers in psychology, 5, 19. https://doi.org/10.3389/fpsyg.2014.00019