Table of Contents

Introduction

The Balanced Scorecard (BSC) approach (Kaplan & Norton, 1996) was a revolutionary book for senior leaders when it was released nearly 25 years ago. Until that time, many senior leaders but especially those in business, focused purely on financial indicators of an organization’s performance. Other Key Performance Indicators (KPI) were either primarily the focus of lower-level managers or directors or not considered at all.

With the BSC approach, you break your indicators into four categories:

- Financial Performance

- Customer Knowledge

- Internal Business Processes

- Learning and Growth

With a more balanced and holistic focus on all the areas your business needs to compete, as opposed to purely focusing on the financial situation you’re in a better position to make strategic decisions that will propel the whole organization forward instead of generating short-term profits at the expense of long-term growth.

{kind=link}

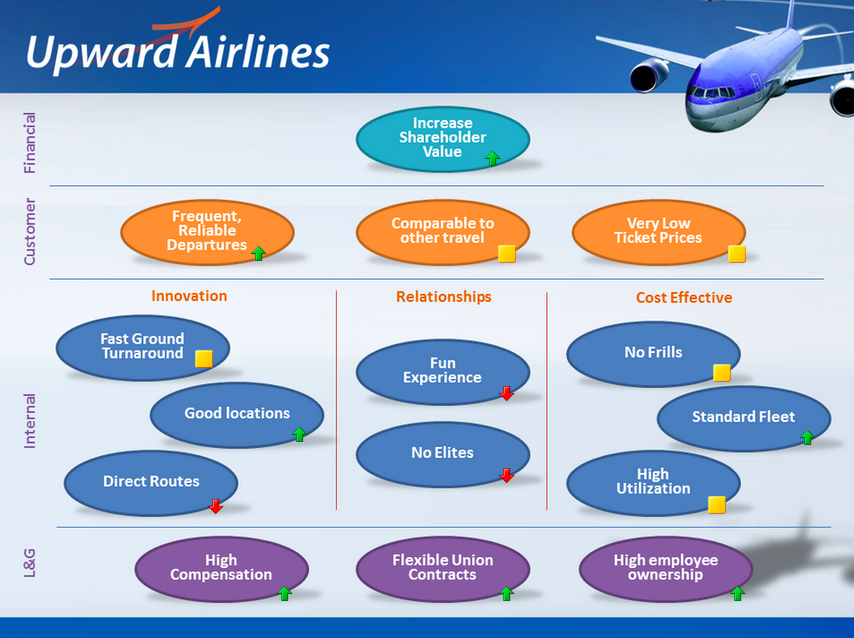

An example from Gomes & Liddle (2009)

Choosing KPIs for Your Balanced Scorecard

It’s important that you choose KPIs that you are truly interested in measuring. There is a tendency for us to choose things that are easy to measure simply because they are, and not because they are actually important for our success. Avoid this seductive trap.

Instead, perform some strategic planning to determine what your actual outcomes are, and once you have those strategic priorities you can begin to map outcomes to them using a logic model.

Financial Performance

This section looks at elements involving your financial performance, as the name suggests. These are the indicators commonly used by executives, which are shrunk from the primary indicators to one of a series. That means selecting only the most highest impact indicators for your organization. These might be:

- Cost per call / per client served

- Ratio of expenses to revenue

- Dollar amount of sales or profit

- Overhead as a percentage of total expenses

Customer Knowledge

This section looks at elements involving your client or customer’s level of success. These elements capture client knowledge of your service, their loyalty to the service and the likelihood that they will promote you or speak of you positively. Some examples might be:

- Number of callers, or percentage growth in callers

- Scores on an external quality survey

- Outcome measures collected from crisis line callers

- Percentage of repeat callers (not because they were dissatisfied but because they appreciated the service and would like it again)

Internal Business Processes

This section looks at elements like efficiency and service delivery. Are there ways to provide the service you provide now, in a way that is more optimized? Examples might be:

- Percentage of calls on a crisis line answered within 30 seconds

- Percentage of follow-up calls made within 24 hours

- Number of clients served at a senior’s eating program

- Scores on internal audits, or percentage of passing audits

Learning and Growth

This section looks at elements like your organization’s culture and access to learning and growth opportunities. How is the culture? How is the bureaucracy? Examples of these items might be:

- Number of policies developed and/or reviewed

- Number of training hours/courses completed

- Percentage of employee receiving 360 degree reviews

- Number or percentage of employees receiving a specific certification (e.g. Certified Crisis Worker, Certified Fund-raising Executive)

Examples of Balanced Scorecards

ClearPoint Strategy provides a number of examples of balanced scorecards on their website, including this graphic which demonstrates the BSC approach as well as the strategy map that places them all on a single page like a dashboard with little icons to indicate their current progress:

{kind=link}

Another example of a Balanced Scorecard is the one from Spectra Community Services (2015). Spectra is a crisis line located west of Toronto in Peel Region. Their BSC, found on page 8 of the linked PDF, uses slightly different headings:

- Help People Cope and Build Resiliency (instead of Customer Knowledge)

- A Great Place to Work and Develop (instead of Learning and Growth)

- Dedicated to Being the Best We Can Be (instead of Internal Processes)

- Operational Excellence (these items also fit under Internal Processes)

- Optimizing Our Resources (instead of Financial Performance)

These headings include a goal, like “Increase total value of funding, in support of organizational goals, i.e. execute fund development plan).” That goal is operationalized, or measured with an item like “$ raised; % of growth year-over-year” and then a target is set, in order to track the results. In this way, the Spectra BSC is a combination of a strategic plan and a scorecard all in one!

References

Gomes, R.C., & Liddle, J. (2009). The balanced scorecard as a performance management tool for third sector organizations: the case of the Arthur Bernardes foundation, Brazil. BAR – Brazilian Administration Review, 6(4), 354-366. https://dx.doi.org/10.1590/S1807-76922009000400006

Kaplan, R.S., Norton, D.P. (1996) The balanced scorecard: turning strategy into action. Brighton, MA: Harvard Business Press.

Spectra Community Support Services. (2015) Strategic Plan 2014-2017 & Balanced Scorecard 2015 Results. Retrieved on September 8, 2019 from https://www.spectrahelpline.org/images/PDF/SPECTRAStrategicPlanAndBalancedScorecard2014-2015.pdf